No interest · No credit check · Repaid on payday

B9 Cash Advance

Get up to $1,000 before payday — no interest, no credit check.

Running short before your paycheck? See in minutes what you could qualify for — then it's repaid automatically on your next payday. No hidden interest, no late fees.

See how much you can get

Answer a few quick questions to check your cash advance options.

By continuing you may be matched with third-party offers and contacted about them. Advance Audit is not a lender and may be paid if you sign up — see our editorial & ad policy.

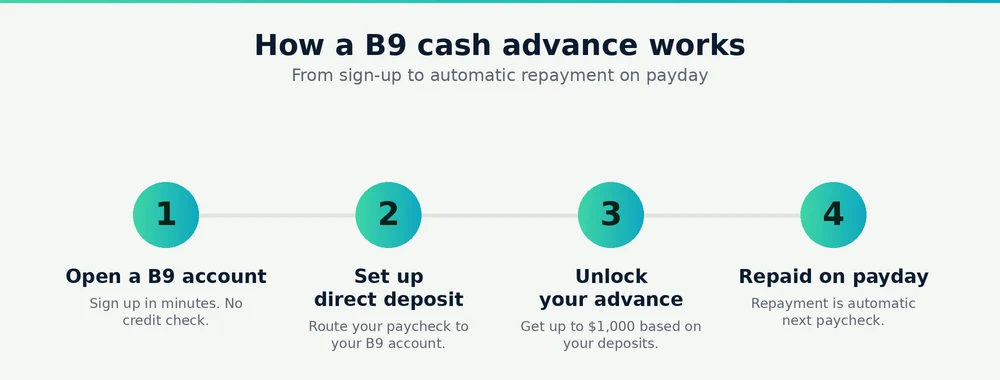

Step by step

How a B9 cash advance works

A B9 advance follows the same four steps every time — here's the full path from opening the app to automatic repayment.

You open a B9 account and route a qualifying direct deposit to it. Once your paycheck lands, B9 unlocks an advance — small at first, then growing toward $1,000 as your deposit history builds. When payday comes around again, the advance is repaid automatically from your incoming deposit, so there's nothing to remember and no late fee. For the full walkthrough see how B9 works and the exact requirements.

Start here

Everything you need to know about B9

Everything we learned first-hand, broken into short, specific answers.

B9: Our Verdict

Hands-on scores, pros and cons, and who B9 is really for.

See verdict → BasicsHow B9 Works

From sign-up to your first advance and automatic repayment, step by step.

How it works → EligibilityB9 Requirements

Income, direct deposit, SSN/ITIN, and the states where B9 isn't available.

Check eligibility → PricingFees & Membership Plans

Basic vs Premium, instant-transfer fees, and how to avoid the monthly cost.

See pricing → LimitsHow Much Can You Get?

Why new users start at $10–$50 and how limits climb toward $1,000.

See limits → TrustIs B9 Legit & Safe?

Who backs the accounts, FDIC insurance, and what real users say.

Is it safe? →Decide with confidence

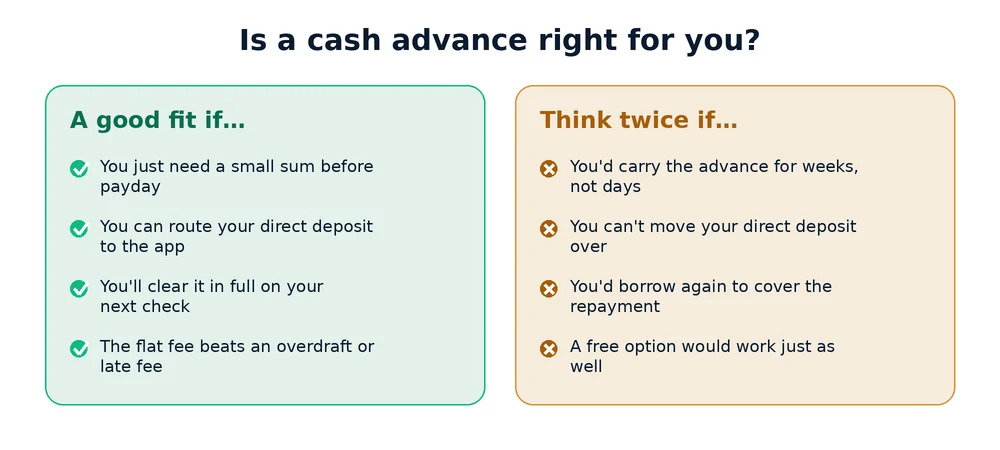

Is a cash advance right for you?

Cash advance apps are genuinely useful in the right situation — and an expensive habit in the wrong one. Use this quick gut-check before you borrow.

The pattern that works: a small shortfall, a paycheck on the way, and a plan to clear the advance in full. The pattern that traps people is rolling one advance straight into the next. If you're unsure of the true cost, run your numbers through our cash advance calculator, and if a fee-free option would do the job, compare apps like B9 first.

The real cost

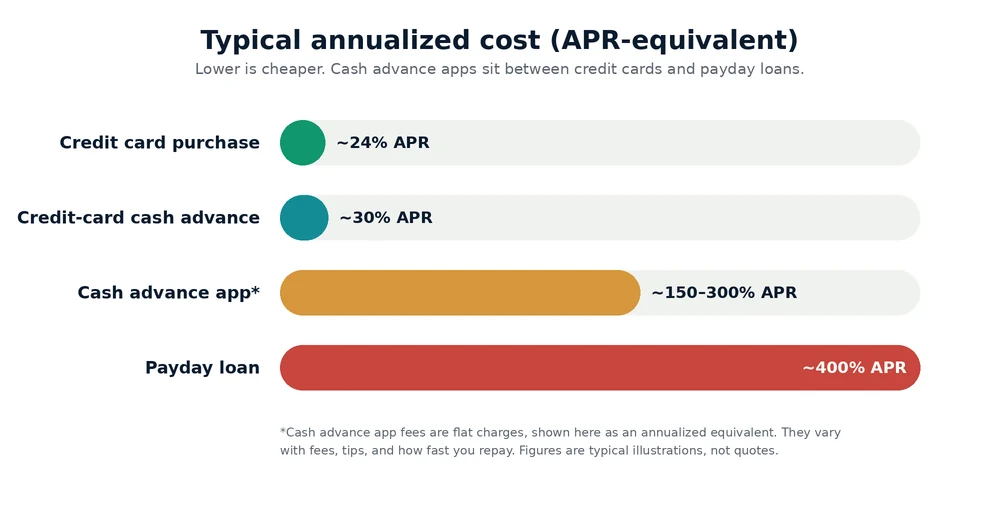

How much does a cash advance really cost?

Flat app fees look tiny next to a credit card — until you annualize them. Here's how a typical advance stacks up against the alternatives.

Because you repay an advance in days rather than a year, a $6 fee can annualize into a triple-digit APR — much cheaper than a payday loan, but far pricier than a credit card. That doesn't make an advance a bad choice; it makes it a tool for short, one-off gaps rather than ongoing borrowing. See where B9's fees come from on the fees & plans page, or estimate your own effective APR with the calculator.

Head to head

B9 vs the other cash advance apps

| App | Max advance | Typical cost | Direct deposit switch? | Best for |

|---|---|---|---|---|

| B9 | $1,000 | $5.99–$19.99/mo membership | Required | Regular users who'll bank with B9 |

| Dave | $500 | ~$1/mo + flat 5% fee ($5–$15) | Not required | Occasional, low-cost advances |

| EarnIn | ~$750/pay period | No required subscription | Not required | Hourly workers who track hours |

| Brigit | $500 | $8.99–$14.99/mo | Not required | Budgeting + credit tools |

Typical published figures as of Jul 2026; limits and fees vary by user and change often — confirm in each app.

Not sold on B9? See every alternative.

We ranked the cash advance apps by real cost, speed, and eligibility — including free options with no direct-deposit requirement.

See apps like B9Why trust Advance Audit

Most write-ups on cash advance apps are rewritten press releases. We do it differently: we create accounts, connect a real bank, request advances, and track every fee that hits the ledger. When a limit or price changes, we update the page and stamp it with the date.

We also tell you when an app isn't the right call. B9 works well for some people and poorly for others, and our full B9 breakdown spells out exactly which is which.

Hands-on · independent

The team behind our B9 testing

We don't rewrite press releases. We open the app, fund an advance, and check every figure before anything is published.

The Advance Audit testing team

Hands-on app testing · Advance Audit

Every figure on this site comes from opening real accounts, funding and repaying real advances, and checking limits, fees, and rules against the live app and current disclosures. Content is team-written and fact-checked before it goes live — and updated with a visible date stamp whenever the product changes.

Read our editorial & ad policy →How we test

- Open a real account and complete identity verification

- Set up direct deposit and fund a live advance

- Itemise every fee, limit, and repayment

- Re-check figures against the live app on every update

No advertiser or partner decides our ratings. See our editorial & ad policy.

Reputation

What B9 users say on Trustpilot

As of Jul 2026 — ratings change, so check the live Trustpilot page.

What reviewers tend to praise

- Fast, convenient advances and getting paid earlier

- Support that many reviewers found quick and helpful

- The credit-building feature and debit cashback

- Simple sign-up and an app that's easy to navigate

Common complaints

- Fees on transfers and everyday transactions

- Direct deposit being switched to B9, or hard to move back

- Funds occasionally held or slow to release

- Account holds/closures and inconsistent support experiences

Overall, B9 keeps a solid 4-star score, and the pattern is consistent with the wider cash-advance category: most people are happy with the speed and convenience, while the recurring frustrations are fees, the direct-deposit requirement, and the occasional support or account issue. We summarise the themes here in our own words — we don't copy or invent individual user posts.

More ways to borrow

If a cash advance isn't enough

A B9 cash advance is built for small, short-term gaps. When you need more — or a longer-term fix — these are the other financing routes worth understanding first.

Beyond a cash advance

Personal Loans

A personal loan gives you a lump sum up front that you repay in fixed monthly installments, usually over two to seven years. Because the rate is fixed, your payment never changes — handy for a planned expense or to replace several smaller debts with one predictable bill. Unlike a B9 cash advance, most personal loans involve a credit check, and your rate depends heavily on your credit profile.

- One fixed monthly payment

- Use the funds for almost any purpose

- Better suited to larger needs than a small advance

Quick facts

- Typical amount

- $1k–$50k

- Term

- 2–7 yrs

- Rate

- ~7%–36% APR

- Credit check

- Yes

General market ranges — not an offer. Actual terms vary by lender and your credit.

For homeowners

Home Equity Loans

If you own your home, a home equity loan lets you borrow against the equity you've built and receive a lump sum at a fixed rate. Because the loan is secured by your property, rates are often lower than unsecured borrowing — but that same security is the risk. It's best reserved for large, planned costs such as renovations or consolidating higher-rate debt.

- Often lower rates than unsecured loans

- Fixed rate and lump sum

- Amount depends on your available equity

Quick facts

- Amount

- Based on equity

- Rate

- Often lower

- Collateral

- Your home

- Best for

- Large costs

General market ranges — not an offer. Actual terms vary by lender and your credit.

Simplify what you owe

Debt Consolidation

Debt consolidation rolls several balances — often high-interest credit cards — into a single loan or payment. The goal is one predictable bill and, ideally, a lower overall interest rate so more of each payment goes toward the principal. It doesn't erase what you owe, but it can make repayment simpler and cheaper if you qualify for a better rate than your current debts.

- Turn many payments into one

- Potential interest savings

- Easier to budget and track

Quick facts

- Combines

- Multiple debts

- Goal

- One lower rate

- Best for

- High-rate cards

- Cuts balance

- No

General market ranges — not an offer. Actual terms vary by lender and your credit.

When you're overwhelmed

Debt Relief

Debt relief covers programs — such as debt settlement or a debt management plan — aimed at reducing or restructuring debt you genuinely can't repay. Settlement tries to negotiate balances down; a management plan reorganizes payments through a counseling agency. These can help in real hardship, but the trade-offs are serious, so weigh them carefully before enrolling.

- May lower the total you owe (settlement)

- Single structured plan (management)

- Consider a nonprofit credit counselor first

Quick facts

- For

- Serious hardship

- Types

- Settle / manage

- Credit impact

- Can be high

- Watch for

- Fees & scams

General market ranges — not an offer. Actual terms vary by lender and your credit.

Answers

B9 cash advance FAQ

The questions people ask most before they sign up.